financial news of interest, including ways to save, investments, insurance, consumer protection, budgeting, retirement, tax tips, paying for college, finding bargains, and starting a business

Articles and news of general interest

about investing, saving, personal finance, retirement, insurance, saving on taxes, college funding, financial literacy, estate planning, consumer education, long term care, financial services, help for seniors and business owners.

The Billion-Dollar Stakes for OpenAI

-

The artificial intelligence giant is closing in on a deal with Microsoft

regarding its future governance, but other questions stand over its huge

costs.

Maximizing Employer Stock Options

-

Oct 29 – On this edition of Lifetime Income, Paul Horn and Chris Preitauer

discuss the benefits of employee stock options and how to best benefit from

th...

✔ Evaluate the tax impact of life changes such as a raise, a new job, marriage, divorce, a new baby, or a child going to college or leaving home.

✔ Check your withholding on your paycheck and estimated tax payments to avoid paying too much or too little.

✔ See if you can contribute more to your 401(k) or 403(b). It is one of the most effective ways to lower your current-year taxable income.

In the midst of your summer fun, taking time for a midyear tax checkup could yield rewards long after your vacation photos are buried deep in your Facebook feed.

Personal and financial events, such as getting married, sending a child off to college, or retiring, happen throughout the year and can have a big impact on your taxes. If you wait until the end of the year or next spring to factor those changes into your tax planning, it might be too late.

“Midyear is the perfect time to make sure you’re maximizing any potential tax benefit and reducing any additional tax liability that result from changes in your life,” says Gil Charney, director of the Tax Institute at H&R Block.

Here are 9 questions to answer to help you be prepared for any potential impacts on your tax return.

1. Did you get a raise or are you expecting one?

The amount of tax withheld from your paycheck should increase automatically along with your higher income. But if you’re working two jobs, have significant outside income (from investments or self-employment), or you and your spouse file a joint tax return, the raise could push you into a higher tax bracket that may not be accounted for in the Form W-4 on file with your employer. Even if you aren’t getting a raise, ensuring that your withholding lines up closely with your anticipated tax liability is smart tax planning. Use the IRS Withholding Calculator; then, if necessary, tell your employer you’d like to adjust your W-4.

Another thing to consider is using some of the additional income from your raise to increase your contribution to a 401(k) or similar qualified retirement plan. That way, you’re reducing your taxable income and saving more for retirement at the same time.

2. Is your income approaching the net investment income tax threshold?

If you’re a relatively high earner, check to see if you’re on track to surpass the net investment income tax (NIIT) threshold. The NIIT, often called the Medicare surtax, is a 3.8% levy on the lesser of net investment income or the excess of modified adjusted gross income (MAGI) above $200,000 for individuals, $250,000 for couples filing jointly, and $125,000 for spouses filing separately. In addition, taxpayers with earned income above these thresholds will owe another 0.9% in Medicare tax on top of the normal 2.9% that’s deducted from their paycheck.

If you think you might exceed the Medicare surtax threshold for 2017, you could consider strategies to defer earned income or shift some of your income-generating investments to tax-advantaged retirement accounts. These are smart strategies for taxpayers at almost every income level, but their tax-saving impact is even greater for those subject to the Medicare surtax.

3. Did you change jobs?

If you plan to open a rollover IRA with money from a former employer’s 401(k) or similar plan, or to transfer the money to a new employer’s plan, be careful how you handle the transaction. If you have the money paid directly to you, 20% will be withheld for taxes and, if you don’t deposit the money in the new plan or an IRA within 60 days, you may owe tax on the withdrawal, plus a 10% penalty if you’re under age 55.

4. Do you have a newborn or a child no longer living at home?

It’s time to plan ahead for the impact of claiming one more or less dependent on your tax return.

Consider adjusting your tax withholding if you have a newborn or if you adopt a child. With all the expenses associated with having a child, you don’t want to be giving the IRS more of your paycheck than you need to.

If your child is a full-time college student, you can generally continue to claim him or her as a dependent—and take the dependent exemption ($4,050 in 2017)—until your student turns 25. If your child isn’t a full-time student, you lose the deduction in the year he or she turns 19. Midyear is a good time to review your tax withholding accordingly.

5. Do you have a child starting college?

College tuition can be eye-popping, but at least you might have an opportunity for a tax break. There are several possibilities, including, if you qualify, the American Opportunity Tax Credit (AOTC). The AOTC can be worth up to $2,500 per undergraduate every year for four years. Different college-related credits and deductions have different rules, so it pays to look into which will work best for you.

Regardless of which tax break you use, here’s a critical consideration before you write that first tuition check: You can’t use the same qualified college expenses to calculate both your tax-free withdrawal from a 529 college savings plan and a federal tax break. In other words, if you pay the entire college bill with an untaxed 529 plan withdrawal, you probably won’t be eligible for a college tax credit or deduction.

6. Is your marital status changing?

Whether you’re getting married or divorced, the tax consequences can be significant. In the case of a marriage, you might be able to save on taxes by filing jointly. If that’s your intention, you should reevaluate your tax withholding rate on Form W-4, as previously described.

Getting divorced, on the other hand, may increase your tax liability as a single taxpayer. Again, revisiting your Form W-4 is in order, so you don’t end up with a big tax surprise in April. Also keep in mind that alimony you pay is a deduction, while alimony you receive is treated as income.

7. Are you saving as much as you can in tax-advantaged accounts?

OK, this isn’t a life-event question, but it can have a big tax impact. Contributing to a qualified retirement plan is one of the most effective ways to lower your current-year taxable income, and the sooner you bump up your contributions, the more tax savings you can accumulate. For 2017, you can contribute up to $18,000 to your 401(k) or 403(b). If you’re age 50 or older, you can make a “catch-up” contribution of as much as $6,000, for a maximum total contribution of $24,000. Self-employed individuals with a simplified employee pension (SEP) plan can contribute up to 25% of their compensation, to a maximum of $54,000 for 2017.

This year’s IRA contribution limits, for both traditional and Roth IRAs, are $5,500 per qualified taxpayer under age 50 and $6,500 for those age 50 and older. Traditional and Roth IRAs both have advantages, but keep in mind that only traditional IRA contributions can reduce your taxable income in the current year.

8. Are your taxable investments doing well?

If your investments are doing well and you have realized gains, now’s the time to start thinking about strategies that might help you reduce your tax liability. Tax-loss harvesting—timing the sale of losing investments to cancel out some of the tax liability from any realized gains—can be an effective strategy. The closer you get to the end of the year, the less time you’ll have to determine which investments you might want to sell, and to research where you might reinvest the cash to keep your portfolio in balance.

9. Are you getting ready to retire or reaching age 70½?

If you’re planning to retire this year, the retirement accounts you tap first and how much you withdraw can have a major impact on your taxes as well as how long your savings will last. A midyear tax checkup is a good time to start thinking about a tax-smart retirement income plan.

If you’ll be age 70½ this year, don’t forget that you may need to start taking a required minimum distribution (RMD) from your tax-deferred retirement accounts, although there are some exceptions. You generally have until April 1 of next year to take your first RMD, but, after that, the annual distribution must happen by December 31 if you want to avoid a steep penalty. So if you decide to wait to take your first RMD until next year, be aware that you’ll be paying tax on two annual distributions when you file your 2018 return.

No significant changes in your life situation or income?

Midyear is still a good time to think about taxes. You might look into ways you can save more toward retirement, gift money to your children and grandchildren to remove it from your estate, or manage your charitable giving to increase its tax benefits and value to beneficiaries. A little tax planning now can save a lot of headaches in April—and maybe for years to come.

Retirement» 7 Little-Known Social Security Benefits

That FICA guy won't be your buddy

In the first season of "Friends," Rachel Green looks at her first paycheck as a waitress and asks, "Who's this FICA guy, and why is he getting all my money?"

That's one hard lesson about Social Security. Another is that when it's time to claim, you can't depend on the Social Security Administration to be your personal adviser.

In an effort to save time and cut costs, Social Security employees generally don't give case-specific advice. So that means you are on your own to make the most important financial decision of a lifetime. You have to read the rules and do the research yourself.

William Meyer, whose website, Social Security Solutions, gives Social Security advice for a fee, says you also can't depend on Social Security to follow instructions you give them electronically. If you have a request that is not the most common choice, you'll need to go to the Social Security office and make the request in person, he says.

There are many ways a married couple can decide to take their Social Security benefits, according to Alicia Munnell, director of the Center for Retirement Research at Boston College. You can't ask Social Security to list them all, so what's the right choice?

Munnell says it's hard to beat waiting until you're 70 to begin benefits because the monthly payment is 76 percent higher than it would be if you had started to take benefits at 62 and 32 percent higher than it would be if you claimed at age 66.

Betting against death

On the other hand, some people advocate drawing Social Security benefits at the first opportunity.

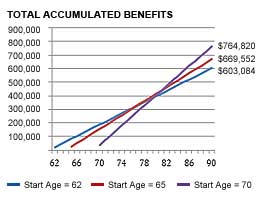

Doug Carey, who founded the financial planning software firm WealthTrace, says Social Security doesn't see itself as an oddsmaker, but it does require you to bet on your longevity. He offers this chart as proof. It graphs the break-even point for a person who earned the inflation-adjusted equivalent of $70,000 per year for 35 years. If this person waits until 70 to claim Social Security and lives until at least age 90, he'll accumulate almost $162,000 more in benefits than he would if he had claimed at 62. But there's a possibility of losing the bet and getting nothing.

Retired law professor and Social Security expert Merton Bernstein says the longevity bet odds are bad, so claim early. "You never know when the bell will ring. I subscribe to the Woody Allen principal: 'Take the money and run.'"

A reward for delaying divorce

If you're not happy in your marriage after 9 1/2 years, hold off before hiring a divorce attorney. "Stay married for at least 10 years," says San Francisco-based Bank of America personal banker Raphael Gilbert. Why? That's what it takes to stake a claim to your ex-spouse's Social Security benefits. If you terminate the marriage after nine years and 11 months, you're out of luck. If you make it for 10 years, you can collect a Social Security benefit based on up to half of your ex's earnings

Bigger reward if ex has 'departed'

And we have another dirty little secret for you. If you haven't remarried, chances are your ex-spouse is worth more to you dead than alive -- especially if he or she was a high earner. Once an ex-spouse passes away, you'll be treated just like a widow or widower. If you are at least 60, you'll be able to collect your late-spouse's benefit and allow your own benefit to grow unclaimed until you reach age 70, when you can switch if your own is higher, according to Carol Thomas, who worked for the Social Security Administration for 28 years and answers questions about Social Security at RetirementCommunity.com.

Assuming your ex will dwell on Planet Earth to a ripe old age, the longer your ex-spouse delays claiming Social Security, the better it is for you. So, if you get a chance, encourage your ex to work until age 70. Then, when it's all over, you'll get to claim half of his or her maximum Social Security. Or once you and your ex-spouse reach full retirement age -- usually 66 -- you can claim half your ex's benefit and let your own grow untouched until you're 70, says Thomas. Consider it payback.

More flexibility for widows and widowers

Social Security does a good job of explaining widow and widower benefits, but Dan Keady, director of financial planning for TIAA-CREF Financial Services, says it doesn't clearly spell out a key difference between widow/widower benefits and spousal benefits. A widow/widower can begin benefits based on his or her own earnings record and later switch to survivors benefits or begin with survivors benefits and later switch to benefits based on his or her own record -- even if the surviving spouse is filing before full retirement age. You can't do that with spousal benefits.

In other words, a widow can begin drawing a survivors benefit on her late husband's Social Security when she is as young as 60, but only at a reduced rate. Then she can choose to leave her own Social Security alone, allowing it to grow in value until her full retirement age -- or even age 70. This works for widowers, too.

SSDI step 1: Hire help

When you apply for disability insurance, Social Security doesn't tell you that your first step ought to be hire a lawyer or other expert adviser. Allsup, a private firm that advises people about how to get SSDI, says Social Security doesn't even make it clear that an applicant can have representation from the very beginning of the application process. As a result, lots of people don't get help until they've been initially denied, and that slows down the process unnecessarily, according to Allsup spokeswoman Mary Jung.

Jung also warns SSDI applicants to be accurate and precise on the application. Small mistakes can make a big difference. Minimizing how much exertion was required to perform the person's job is a common mistake that frequently results in denial of a claim.

35 years is the magic number

The Social Security website offers an explanation of how your benefits are calculated, but it's a little hard to follow. You can find a simpler explanation at MyRetirementPaycheck.org, a website sponsored by the National Endowment for Financial Education.

Your Social Security payment is figured using a complex calculation based on a 35-year average of your covered wages. Each year's wages are adjusted for inflation before being averaged. If you worked longer than 35 years, the government will use the highest 35 years. If you worked for less than 35 years, they'll average in zeros for the years you are lacking. You don't have to be a math genius to figure out the impact of that -- it drags down your average. If you can avoid zeros by working a couple of years longer, you'll increase your Social Security payment.

1. In general, what requirements must be met to qualify a person for retirement benefits?

An individual is entitled to a retirement benefit if he or she: (1) is fully insured, (2) is at least age 62 throughout the first month of entitlement, and (3) has filed an application for retirement benefits.

2. Must a person be fully insured to qualify for retirement benefits?

Yes. (But a small monthly benefit is payable to some men who became age 72 before 1972 and some women who became age 72 before 1970).

3. What is the earliest age at which a person can start to receive retirement benefits?

Age 62. A retired worker who is fully insured can elect to start receiving a reduced benefit at any time between ages 62 and full retirement age (which is gradually increasing from 65 to 67; see below) when he would receive the full benefit rate. A person is not required to be completely retired to receive retirement benefits. A person is considered “retired” if the retirement test is met.

The retirement age when unreduced benefits are available (previously age 65) increased by two months per year for workers reaching age 62 in 2000-2005. It is age 66 for workers reaching age 62 in 2006-2016. It will increase again by two months per year for workers reaching age 62 in 2017-2022. Finally, the retirement age will be age 67 for workers reaching age 62 after 2022 (i.e., reaching age 67 in 2027).

The full retirement age for spouse’s benefits (also previously age 65) moves upward in exactly the same way as that for workers. The full retirement age for widow(er)’s benefits also rises but in a slightly different manner (beginning for widow(er)s who attain age 60 in 2000 and reaching a full retirement age of 67 in 2029).

Reduced benefits will continue to be available at age 62, but the reduction factors are revised so that there is a further reduction of up to a maximum of 30% for workers entitled at age 62 after the retirement age is increased to age 67 (rather than only 20% for entitlement at age 62 under previous law).

4. Must a person file an application for retirement benefits?

Yes. A person can file an application within three months before the first month in which he becomes entitled to benefits. The earliest date for filing would be three months before the month of attaining age 62.

As evidence of age, a claimant must ordinarily submit one or more of the following: birth certificate; church record of birth or baptism; Census Bureau notification of registration of birth; hospital birth record; physician’s birth record; family Bible; naturalization record; immigration record; military record; passport; school record; vaccination record; insurance policy; labor union or fraternal record; marriage record; other evidence of probative value.

If a person is receiving Social Security disability benefits for the month before the month he reaches full retirement age, no application is required; the disability benefit ends and the retirement benefit begins automatically.

5. What is the amount of a retirement benefit?

A retirement benefit that starts at full retirement age (see Q 31) equals the worker’s Primary Insurance Amount (PIA). But a worker who elects to have benefits start before full retirement age will receive a monthly benefit equal to only a percentage of the PIA. The PIA will be reduced by 5/9 of 1% for each of the first 36 months the worker is under full retirement age when payments commence and by 5/12 of 1% for each such month in excess of 36.

As a general rule, a person taking reduced retirement benefits before full retirement age will continue to receive a reduced rate after normal retirement age.

An individual can obtain higher retirement benefits by working past full retirement age.

6. What is the first month for which a retired person receives a retirement benefit?

A monthly benefit is available to a retired worker when he reaches age 62, provided he is fully insured.

Workers and their spouses (including divorced spouses) do not receive retirement benefits for a month unless they meet the requirements for entitlement throughout the month. The major effect of this provision is to postpone, in the vast majority of cases, entitlement to retirement benefits for persons who claim benefits in the month in which they reach age 62 to the next month. Only in the case of a person who attains age 62 on the first or second day of a month can benefits be paid for the month of attainment of age 62. Note that a person attains his age on the day preceding the anniversary of his birth. For example, if an individual was born on May 2, 1951, he is considered 62 years old on May 1, 2013.

Most entitlement requirements (other than the entitlement of the worker) affecting young spouses or children of retired or disabled workers are deemed to have occurred as of the first of the month in which they occurred. However, in the case of a child who is born in or after the first month of entitlement of a retired or disabled worker, benefits are not payable for the month of birth (unless born on the first day of the month).

Retroactive benefits are usually prohibited if permanently reduced benefits (as compared with what would be payable for the month the application is filed) would occur in the initial month of eligibility. However, retroactive benefits may be applied for if: (1) with respect to widow(er)’s benefits, the application is for benefits for the month of death of the worker, if filed for in the next month, and (2) retroactive benefits for any month before attaining age 60 are applied for by a disabled widow(er) or disabled surviving divorced spouse.

7. Can a person receive retirement benefits regardless of the amount of his wealth or the amount of his retirement income?

Yes, a person is entitled to retirement benefits regardless of how wealthy he is. Also, the amount of retirement income a person receives (e.g. dividends, interest, rents, etc.) is immaterial. A person is subject to loss of benefits only because of excess earnings arising from his personal services.

8. Can a person lose retirement benefits by working?

Yes, a person can lose some or all monthly benefits if she is under the full retirement age (see Q 31) for all of 2014 and his or her earnings for the year exceed $15,480. A person may lose benefits if she reaches full retirement age in 2014 and if she earns over $41,400, but only those earnings earned before the month he or she reaches full retirement age count towards the $41,400 limit. The amount of loss depends on the amount of earnings in excess of these earnings limits. In no case will a person lose benefits for earnings earned after reaching full retirement age. For the initial year of retirement of a person who is under the full retirement age for all of 2014, the monthly earnings limit is $1,290. For purposes of this test, “earnings” include not only earnings in covered employment, but also earnings in noncovered employment in theUnited States. As to noncovered employment outside theUnited States, benefits are lost for any month before reaching full retirement age when so employed for more than 45 hours, regardless of the amount of earnings.

The dollar exempt amounts mentioned above will be increased automatically after 2014 as wage levels rise.

9. When do retirement benefits end?

At the worker’s death. No retirement benefit is paid for the month of death.

10. Can a husband and wife both receive retirement benefits?

Yes. If each is entitled to receive benefits based on his or her own earnings record, each can receive retirement benefits independently of the other’s benefits. However, a woman or man who is entitled to a retirement benefit and a spouse’s benefit cannot receive both in full.

11. Is the spouse of a retired or disabled worker entitled to benefits?

An individual is entitled to spouse’s benefits on a worker’s Social Security record if:

The worker is entitled to retirement or disability benefits; and

The individual has filed an application for spouse’s benefits; and

The spouse is not entitled to a retirement or disability benefit based on a primary insurance amount equal to or larger than one-half of the worker’s primary insurance amount; and

The spouse is either age 62 or over, or has in their care a child under age 16, or disabled, who is entitled to benefits on the worker’s Social Security record.

The spouse of a worker must also meet one of the following conditions: (1) the spouse must have been married to the worker for at least one year just before filing an application for benefits; (2) the spouse must be the natural mother or father of the worker’s biological child; (3) the spouse was entitled or potentially entitled to spouse’s, widow(er)’s, parent’s, or childhood disability benefits in the month before the month of marriage to the worker; or (4) the spouse was entitled or potentially entitled to a widow(er)’s, parent’s, or child’s (over 18) annuity under the Railroad Retirement Act in the month before the month of marriage to the worker. A spouse is “potentially entitled” if he or she meets all the requirements for entitlement other than the filing of an application and attaining the required age.

12. What is meant by having a child “in care”?

Having a child in care is a basic requirement for spouse’s benefits when the spouse is under age 62 and for mother’s and father’s benefits. “In care” means that the mother or father: (1) exercises parental control and responsibility for the welfare and care of a child under age 16 or mentally incompetent child age 16 or over, or (2) performs personal services for a disabled mentally competent child age 16 or over.

13. Is the divorced spouse of a retired or disabled worker entitled to a spouse’s benefits?

The spouse is entitled to a divorced spouse’s benefit on the worker’s Social Security record if: (1) the worker is entitled to retirement or disability benefits, (2) the spouse has filed an application for divorced spouse’s benefits, (3) the spouse is not entitled to a retirement or disability benefit based on a primary insurance amount that equals or exceeds one-half the worker’s primary insurance amount, (4) the spouse is age 62 or over, (5) the spouse is not married, and (6) the spouse was married to the worker for at least 10 years before the date the divorce became final.

A divorced spouse who is age 62 or over and who has been divorced for at least two years is able to receive benefits based on the earnings of a former spouse who is eligible for retirement benefits, regardless of whether the former spouse has retired or applied for benefits. This two-year waiting period for independent entitlement to divorced spouse’s benefits is waived if the worker was entitled to benefits prior to the divorce. A spouse whose divorce took place after the couple had begun to receive retirement benefits, and whose former spouse (the worker) returned to work after the divorce (thus causing a suspension of benefits), will not lose benefits on which he or she had come to depend.

14. What is the amount of a spouse’s benefit?

If the spouse of a retired or disabled worker is caring for the worker’s child under age 16 or disabled child, the monthly benefit equals half of the worker’s PIA, regardless of his age. If the spouse is not caring for a child, monthly benefits starting at full retirement age likewise equal half of the worker’s PIA; but if the spouse chooses to start receiving benefits at or after age 62, but before full retirement age, the benefit is reduced.

If the spouse chooses to receive, and is paid, a reduced spouse’s benefit for months before full retirement age, the spouse is not entitled to the full spouse’s benefit rate upon reaching full retirement age. A reduced benefit rate is payable for as long as the spouse remains entitled to spouse’s benefits.

A spouse will not always receive a spouse’s full benefit; under the following circumstances a spouse will receive a smaller amount:

(1) If the total amount of monthly benefits payable on the worker’s Social Security account exceeds the Maximum Family Benefit, all benefits (except the worker’s benefit) will be reduced proportionately to bring the total within the family maximum limit.

(2) If a spouse who is not caring for a child elects to start receiving a spouse’s benefit at age 62 (or at any time between age 62 and full retirement age), the benefit will be reduced by 25/36 of 1% for each of the first 36 months that the spouse is under full retirement age when benefits commence, and by 5/12 of 1% for each such month in excess of 36.

(3) If the spouse is entitled to a retirement or disability benefit that is smaller than the spouse’s benefit rate, the spouse will receive a spouse’s benefit equal to only the difference between the retirement or disability benefit and the full spouse’s benefit rate.

(4) The amount of a spouse’s monthly benefit is usually reduced if the spouse receives a pension based on his or her own work for a federal, state, or local government that is not covered by Social Security on the last day of such employment. However, the Social Security Protection Act of 2004 generally requires that a person work in a situation covered by Social Security for five years to be exempt from this Government Pension Offset (GPO).

If a spouse is entitled to a retirement or disability benefit that is larger than the spouse’s benefit rate, he or she will receive only the retirement or disability benefit.

15. What is the amount of a divorced spouse’s benefit?

The amount of a divorced spouse’s benefit is the same as a spouse’s benefit amount. As a general rule, it will equal half of the beneficiary’s former spouse’s PIA and will be reduced if he or she elects to start receiving benefits before normal retirement age. However, a divorced spouse’s benefit is paid independently of other family benefits. In other words, it will not be subject to reduction because of the family maximum limit, and will not be taken into account in figuring the maximum limit for the former spouse’s family.

16. Must a spouse be dependent upon the worker for support to be eligible for a spouse’s benefits?

No, a spouse is entitled to benefits if the worker is receiving benefits and the spouse is otherwise qualified. A spouse need not be dependent upon the worker, and may be independently wealthy.

17. May a spouse lose benefits if the worker works or if the spouse works?

Yes, a spouse can lose some or all of his or her monthly benefits if the worker is under the full retirement age for the entire year and earnings exceed $15,480 (in 2014). A spouse may also lose benefits in the year the worker reaches full retirement age if the worker earns over $41,400 (in 2014), but only earnings earned before the month the worker reaches full retirement age count towards the $41,400 limit. Similarly, if the spouse is under full retirement age for the entire year and has earnings of over $15,480 (or earnings of over $41,400 in the year that full retirement age is attained), some or all benefits can be lost.

When both the worker and the spouse have earnings in excess of the earnings limitation: (1) 50% of the worker’s “excess” earnings are charged against the total monthly family benefits if the worker is under the full retirement age, and 33⅓% in the year the worker is to reach the full retirement age, and then (2) the spouse’s “excess” earnings are charged against his or her own benefits in the same manner, depending upon the age of the spouse, but only to the extent that those benefits have not already been charged with the worker’s excess earnings. Example. Mr. Smith, age 62 on January 1, 2014, is entitled to a monthly retirement benefit of $346, and his wife, also age 62 on January 1, 2014, is entitled to a monthly spouse’s benefit of $162. Mr. Smith had earnings that were $4,064 in excess of the earnings limitation. His wife had earnings that were $1,620 in excess of the earnings limitation. Mr. Smith’s earnings are charged against the total monthly family benefit of $508 ($346 + $162), so neither Mr. Smith nor his wife receives payments for January through April (50% of $4,064 = $2,032, and 4 × $508 = $2,032). The wife’s excess earnings are charged only against her own benefit of $162. As her benefits for January through April were charged with the worker’s excess earnings, the charging of her own earnings cannot begin until May; she thus receives no benefits for May through September (50% of $1,620 = $810, and 5 × $162 = $810). Exception. The excess earnings of the worker do not cause deductions from the benefits of an entitled divorced spouse who has been divorced from the worker at least two years or whose former spouse was entitled to benefits before the divorce.

18. When does a spouse’s benefit end?

A spouse’s benefits end when: (1) the spouse dies; (2) the worker dies (in this case, the spouse will be entitled to widow(er)’s, mother’s, or father’s benefits); (3) the worker’s entitlement to disability benefits ends and he or she is not entitled to retirement benefits (unless the divorced spouse meets the requirements for an independently entitled divorced spouse); (4) the spouse is under age 62 and there is no longer a child of the worker under 16 or disabled who is entitled to child’s benefits; (5) the spouse becomes entitled to retirement or disability benefits and his or her PIA is equal to or larger than one-half of the worker’s PIA; (6) the spouse and the worker are divorced before the spouse reaches age 62 and before the spouse and worker had been married for 10 years; or (7) the divorced spouse marries someone other than the worker. However, the divorced spouse’s benefit will not be terminated by marriage to an individual entitled to widow(er)’s, mother’s, father’s or parent’s monthly benefits, or to an individual age 18 or over who is entitled to childhood disability benefits.

A spouse is not entitled to a spouse’s benefit for the month in which any of the above events occurs. The last payment will be the payment for the preceding month.

19. Will a spouse’s benefit be reduced if the spouse is receiving a government pension?

Social Security benefits payable to spouses – including surviving spouses and divorced spouses – are reduced (but not below zero) by two-thirds of the amount of any governmental (federal, state, or local) retirement benefit payable to the spouse based on his or her own earnings in employment not covered by Social Security, if that person’s last day of employment was not covered by Social Security (but see below for SSPA 2004). Thus, for the affected group, the spouse’s benefit is reduced $2 for every $3 of the government pension.

The Social Security Protection Act of 2004 (SSPA 2004) requires a person to work in covered employment for the last 60 months (instead of one day) of employment to be exempt from the government pension offset (GPO). This change will not apply to someone whose last day of government service was beforeJuly 1, 2004. Also, the required 60 months will be reduced for each month of government service that was covered by Social Security before the enactment of SSPA 2004. These reduced months of service must be performed after enactment.

This offset against Social Security benefits did not apply prior to December 1977, or if the individual: (1) met all the requirements for entitlement to Social Security benefits that existed and were applied in January 1977, and (2) received or was eligible to receive a government pension between December 1977 and December 1982. In addition, it does not apply to those first eligible to receive a government pension prior to July 1983 if they also meet the one-half support test.

Generally, federal workers hired before 1984 are part of the Civil Service Retirement System (CSRS) and are not covered by Social Security. Most Federal workers hired after 1983 are covered by the Federal Employees’ Retirement System Act of 1986 (FERS), which includes coverage by Social Security. The FERS law provided that employees covered by the CSRS could, from July 1, 1987 to December 31, 1987, make a one-time election to join FERS (and thereby obtain Social Security coverage). Thus, a CSRS employee who switched to FERS during this period immediately became exempt from the government pension offset. Also, an employee who elected FERS on or before December 31, 1987is exempt from the government pension offset, even if that person retired from government service before his FERS coverage became effective.

However, federal employees who elect to become covered under FERS during any election period which may occur on or afterJanuary 1, 1988, are exempt from the government pension offset only if they have five or more years of federal employment covered by Social Security after January 1, 1988. This rule also applies to certain legislative branch employees who first become covered under FERS on or afterJanuary 1, 1988. Pensions based wholly on service performed as a member of a uniformed service, whether on active or inactive duty, are excluded from the offset.

20. What is the best time to file for Social Security retirement benefits?

The decision on when to apply for Social Security retirement benefits depends on a number of factors. Taking benefits early (before full retirement age) will result in a permanent reduction of benefits. Taking retirement benefits later will result in a high benefit amount, but a shorter life may result in lower total benefits. The Social Security Administration provides a Retirement Planner on its website which includes a number of calculators to help a person determine the right time to file for benefits and the effect on benefits of filing early or late.

However, the federal government does allow an individual a “re-do” if he or she decides that the application for retirement benefits was made too early. By filing Form 521, an individual can request that the original application for retirement benefits be withdrawn and a new application date be substituted. The catch is that the individual must pay back all retirements benefits received up to the date of the withdrawal. However the federal government does not charge a penalty or interest for filing a Form 521, but the individual must have the cash to repay the federal government.

Another consideration on for when to take retirement benefits is how much income will be earned in the year for which benefits are applied. Too much earned income will result in a loss of benefits .

Additionally, since Social Security benefits may be subject to income taxation the individual’s income and tax situation should be considered.

21. When should a person file for retirement benefits?

A person should get in touch with a Social Security office two or three months before reaching age 62. The Social Security office will furnish the information needed to decide whether or not to file an application for retirement benefits at that time. Because of the rules regarding retroactive benefits, a person should consider filing for benefits on January 1 of the year that he or she attains Full Retirement Age (FRA).

If a worker does not file an application, he should contact the Social Security office again: (1) two or three months before retirement; (2) as soon as the worker knows that he will neither earn more than the monthly exempt amount in wages nor render substantial services in self-employment in one or more months of the year, regardless of expected total annual earnings; or (3) two or three months before the worker reaches FRA, even if still working.

It may be advantageous to delay filing an application for benefits where: (1) the person is under the FRA and wishes to wait and receive an unreduced benefit at FRA, (2) the person is at the FRA but benefits are not payable because of earnings (application at or near retirement may provide higher benefits in the year of retirement), or (3) the person would lose benefits payable under some other program.

22. If age 62 is the computation age, is there any advantage to waiting until normal retirement age to collect benefits?

Yes, the full PIA is payable at full retirement age, with a reduced amount paid in case of an earlier retirement age. Age 62 is used to determine elapsed years but earnings are counted to full retirement age. Thus, early retirement usually affects the benefit in two ways. The PIA usually will be smaller (because fewer years of possibly higher earnings will be used in computing the AIME), and the lower PIA will be subject to reduction (5/9 of 1% per month for the first 36 months under the full retirement age and 5/12 of 1% per month for any additional months under the full retirement age).

23. Can a person obtain higher retirement benefits by working past retirement age?

Yes, in two ways.

First, workers who continue on the job receive an increase in retirement benefits for each year they work between full retirement age and 70. Note that this is not an increase in the worker’s PIA. Other benefits based on the PIA, such as those payable to a spouse, are not affected.

This delayed retirement credit is also payable to a worker’s surviving spouse receiving a widow(er)’s benefit.

Beginning in 1990, the delayed retirement credit payable to workers who attain age 62 after 1986 and who delay retirement past the full retirement age, the full-benefit age (gradually rising from age 65 to age 67) is gradually increased. The delayed retirement credit is increased by one-half of 1% every other year until reaching 8% per year in 2009 or later. The higher delayed retirement credits are based on the year of attaining age 62 and are payable only at and after full retirement age.

Delayed Retirement Credit Rates

Attain Age 62

Monthly Percentage

Yearly Percentage

1979-1986

1/4 of 1%

3%

1987-1988

7/24 of 1%

3.50%

1989-1990

1/3 of 1%

4%

1991-1992

3/8 of 1%

4.50%

1993-1994

5/12 of 1%

5%

1995-1996

11/24 of 1%

5.50%

1997-1998

1/2 of 1%

6%

1999-2000

13/24 of 1%

6.50%

2001-2002

7/12 of 1%

7%

2003-2004

5/8 of 1%

7.50%

2005 or after

2/3 of 1%

8%

Workers, who became age 65 before 1990 (and after 1981) and continued on the job, received an increase in retirement benefits usually equal to 3% for each year (1/12 of 3% for each month) they worked between age 65 and 70. (The factor was only 1% for workers who became age 65 before 1982.)

Second, working past the full retirement age frequently results in a higher AIME. The reason: In figuring the number of years to be used in the computation, the year in which the person reaches age 62 and succeeding years are not counted. But those years can be selected as years of highest earnings.

24. Will the retirement age at which unreduced benefits are available ever be increased?

Yes, the Social Security Amendments of 1983 increased the full retirement age (the age at which unreduced benefits are available), by two months per year for workers reaching age 62 in 2000-2005 – to age 66; maintained age 66 for workers reaching age 62 in 2006-2016; increased by two months a year the retirement age for workers reaching age 62 in 2017-2022; and maintained age 67 for workers reaching age 62 after 2022. It does not change the age of eligibility for Medicare.

The 1983 amendments do not change the availability of reduced benefits at 62 (60 for widow(er)s), but revise the reduction factors so that there is a further reduction (up to a maximum of 30% for workers entitled at age 62 after the full retirement age is increased to age 67, rather than only up to 20% for entitlement at age 62 under prior rules). There is no increase in the maximum reduction in the case of widow(er)s, but some increases in the reduction occur at ages over 60 and under full retirement age.

Effects of Retirement-Age Provision in Social Security Amendments of 1983*

Year of Birth

Attainment of Age 62

Full Retirement Age (Year/Months)

Date of Attainment of Full Retirement Age1

Age-62 Benefit as Percent of PIA2

1938

2000

65/2

March 1, 2003

79.2

1939

2001

65/4

May 1, 2004

78.3

1940

2002

65/6

July 1, 2005

77.5

1941

2003

65/8

September 1, 2006

76.7

1942

2004

65/10

November 1, 2007

75.8

1943-1954

2005-2016

66/0

January 1, 2009-2020

75.0

1955

2017

66/2

March 1, 2021

74.2

1956

2018

66/4

May 1, 2022

73.3

1957

2019

66/6

July 1, 2023

72.5

1958

2020

66/8

September 1, 2024

71.7

1959

2021

66/10

November 1, 2025

70.8

1960 and after

2022 and after

67/0

January 1, 2027 and after

70.0

* Full retirement age is for worker and spouse benefits only. Full retirement age for widow(er)s is based on attainment of age 60 in 2000 or later, so that Full retirement age is age 67 beginning 2029.

1 Birth date assumed to be January 2 of year (for benefit-entitlement purposes, the Social Security Administration considers a person to reach a given age on the day before the anniversary of his birth, thus, someone born on the 1st of the month is considered to reach a given age on the last day of the previous month). For later months of birth, add number of months elapsing after January up to birth month.

2 Applies present-law reduction factor (5/9 of 1 percent per month) for the first 36 months' receipt of early retirement benefits and new reduction factor of 5/12 of 1 percent per month for additional months.

The content in this article is not intended or written to be used, and it cannot be used, for the purposes of avoiding U.S. tax penalties.

All materials on this site are copyrighted by the National Underwriter Company. Distribution of these copyrighted materials to those who have not purchased the book is prohibited.

The above article was drawn from 2014 Social Security & Medicare Facts, and originally published by The National Underwriter Company, a Summit Professional Networks business as well as a sister division of LifeHealthPro.

Money & Investing

Rewrite Your Will Janet Novack and Ashlea Ebeling 01.17.11, 6:00 PM ET

Over the pained howls of liberals, Congress has increased the exemption from the federal estate tax to $5 million, leaving fewer than 4,000 families likely to be stuck paying the 35% tax in 2011. While the new estate deal expires at the end of 2012, the $5 million figure is unlikely to fall. "Rates can fluctuate, but estate tax exemptions don't get reduced," says Columbia Law School professor Michael J. Graetz, who coauthored a book on the political battle over taxing inherited wealth.

That hefty $5 million exemption, combined with a new portability provision, should allow many affluent couples to simplify their planning, leaving their assets outright to each other instead of to cumbersome bypass trusts. Portability? If a married person dies in 2011 or 2012 without using up his full $5 million exemption (amounts left to charity or a U.S. citizen spouse are estate tax free and don't count against that exemption), the unused exemption is passed to the surviving spouse. That allows a widow or widower to leave as much as $10 million free of estate tax. (No, before you entertain lurid ideas, you can't stockpile multiple spousal exemptions through serial marriages. Only what is left of your last late spouse's exemption counts.) Here's a look at what you need to know and do in 2011.

Don't ignore the basics

Whatever your age, marital status or net worth, you need a will (saying who gets your stuff); a living will (stating your wishes about end-of-life care); a health care proxy (naming someone to make medical decisions for you if you can't); and a durable power of attorney (designating someone to act on your behalf in financial and legal matters if you can't). If your situation is very simple and you are cheap, using do-it-yourself software is better than nothing. (More than half of Americans lack wills.) If you have minor or disabled children, or substantial assets, or live in a state with its own version of an estate tax, spring for a lawyer.

Review any old estate plans

"People are going to have to undo a lot of the planning that's been done,'' warns Bernard Kent, a lawyer, CPA and managing director of Telemus Capital Partners in Southfield, Mich. Example: Many couples have old wills designed mainly to preserve the estate tax exemption of the first spouse to die, something the law now does. Under these old "formula" wills, when the first spouse dies assets equal to his or her federal estate exemption go into a "bypass trust" for their kids. The surviving spouse has access to the trust's earnings and, if need be, principal, but what's in the trust "bypasses" the survivor's estate. Problem is, with the exemption jumping to $5 million (it was only $2 million in 2008) the survivor could be left with nothing outside the trust. Moreover, individual retirement accounts, primary residences and other assets that shouldn't be in the trust for income tax reasons could be automatically sucked in, warns Portland, Ore. estate lawyer Marsha Murray-Lusby.

But don't be too quick to write off all trusts, she adds. Couples in a second marriage will want a fixed amount in a bypass trust to make sure kids from their first marriages aren't stiffed. A bypass trust can also provide valuable asset protection--a consideration if, for example, the surviving spouse is an architect, obstetrician or some other professional who could face big legal claims.

Still, many couples in stable first marriages might sensibly opt to leave everything to each other outright (with an "I love you" will) and include a backup "disclaimer" trust for the kids. With this setup, at the death of a spouse the surviving widow or widower can decide, based on the laws and the couple's assets at that time, which assets, if any, to disclaim (turn down) and divert into the kids' trust.

-- Plan for state taxes

Currently 21 states and the District of Columbia have estate or inheritance taxes, or both, in place for 2011. Estate taxes are levied on any amount above an exemption--typically $1 million--left to someone other than a spouse. Inheritance taxes are based on who gets the cash and can hit the first dollar of a bequest. So, for example, Maryland imposes an estate tax of up to 16% above a $1 million exemption and a 10% inheritance tax on every dollar left to a niece, nephew, friend or lover, but not on money left to children, grandchildren, parents or siblings. (Any estate tax owed is reduced by the inheritance tax paid.)

Bottom line: Couples worth $2 million or more living in Maine, Maryland, Massachusetts, Minnesota, New York and Oregon, which all have $1 million state estate tax exemptions, will still want to put at least $1 million in a bypass or disclaimer trust at the first spouse's death.

For details on your own state's estate tax exemption for 2011, see the Forbes Tax Map.

Give while you're still breathing

As in past years you can make annual gifts of up to $13,000 to as many people as you want without worrying about gift taxes. If you want to give even more, there's a lifetime gift tax exemption that jumps to $5 million in 2011 and 2012, up from $1 million in 2010. (The estate tax lapsed in 2010, but the gift tax didn't. Any gift tax exemption used reduces an individual's estate tax exemption.) The generation-skipping transfer tax, an extra tax on gifts and bequests to grandkids if their parents are still alive, also now has a $5 million exemption, up from $1 million in 2009.

When that $5 million gift/GST exemption is leveraged with such fancy wealth-transfer techniques as grantor-retained annuity trusts and installment sales to trusts, the rich will be able to transfer huge sums, tax free, to trusts for their kids, grandkids and generations beyond. (Dynasty trusts, they're called.) "This is a huge gimme to the wealthy,'' says Jonathan Forster, an estate lawyer with Greenberg Traurig, in McLean, Va. Since GRATs and other techniques could be restricted when Congress finally goes into deficit-cutting mode and since the GST tax exemption isn't portable between spouses, lawyers are advising the very rich to begin transferring assets in 2011.

Less wealthy folks can make good use of the gift exemption, too--to avoid state taxes. Oddly most states with inheritance and/or estate taxes don't tax gifts. (The big exception is Tennessee, which imposes up to a 16% tax on gifts above $13,000 a year to close relatives and above $3,000 to others.) So if you have enough left for your own retirement years, you can start reducing prospective state tax bills by making gifts. This is also a boon for unmarried couples who want to transfer assets between partners. Be careful, however, of quirky state gotchas; for example, in Maryland, gifts made within two years before the donor's death get hit with state inheritance but not state estate tax, says Rockville, Md. lawyer Steven Widdes.

Keep income taxes in mind

Under the 2011 and 2012 estate tax law (and likely in the future, too) at your death, all your assets are "stepped up" to their current market value--meaning heirs can sell right away without owing capital gains tax. So don't give away already appreciated assets (say a primary or vacation home or collectibles) you might otherwise hold until death.

On the other hand, the $5 million gift tax exemption provides an opportunity to shift income to relatives taxed at lower rates. Got $30,000 worth of Google stock you bought for $10,000 and are ready to dump? Give it to your starving-artist daughter and she can sell it at a 0% capital gains tax rate in 2011 or 2012. (Warning: Full-time students up to age 24 are subject to the kiddie tax, which taxes investment income and gains at a parent's higher rate.)

CPA Robert Keebler of Green Bay, Wis. suggests the owner of a profitable small business run as a pass-through (the business doesn't pay corporate income taxes but passes all profit through to its owners' tax returns) consider gifting partial ownership stakes to adult children, who might pay taxes on their share of profits at, say, a 25% rate, instead of the 35% the parents pay. "The income-shifting opportunities are enormous," he says.

6 ways to get more Social Security Marriages -- even former ones -- can have significant financial advantages. Here's a look at how having said 'I do' can win you more in retirement benefits.

By U.S. News & World Report

Couples who are currently married, or who have stayed together at least 10 years, tie together their working records -- and the resulting Social Security checks -- as long as they both shall live.

In the case of Social Security payments, the result is often better for the couple than it would have been for a single person. Spouses have Social Security claiming options that single people don't. Here are a few ways couples can boost their Social Security benefits:

1. Utilize spousal payments. Spouses are entitled to a Social Security payout of up to 50% of the higher earner's check (if that amount is higher than benefits based on his or her own working record). Retired couples in which one spouse didn't work or had low earnings have the most to gain from this provision.

However, low-earning spouses must wait until the full retirement age, as the Social Security Administration calls it, to collect the full 50%. Benefits are reduced for spouses who collect before their full retirement age. (For baby boomers born from 1943 to 1954, the full retirement age is 66.)

For example, a low-earning spouse whose full retirement age is 66 would be eligible for only 35% of the higher earner's benefit at age 62. The spousal benefit does not increase above 50% of the higher earner's benefit if claiming is delayed beyond the full retirement age.

2. Claim and suspend. The low-earning spouse cannot receive spouse's benefits until the higher earner files for retirement benefits. Workers who have reached their full retirement age may apply for retirement benefits and then request to have the payment suspended. Claiming and suspending payments allows the lower earner to claim a spousal benefit and the higher earner to continue working and earn delayed retirement credits until age 70.

"This would tend to maximize their lifetime benefits and, more importantly, maximizes the survivor's benefit," says Andrew Biggs, a resident scholar at the American Enterprise Institute and a former deputy commissioner of the Social Security Administration. "You will ensure you will have a higher benefit when you need one, which is when you are a widow later in life."

Social Security checks increase by 7% to 8% for each year of delayed claiming between your full retirement age and age 70. After age 70, there is no additional benefit for waiting to collect your due.

3. Claim twice. Spouses in dual-earner marriages who have reached their full retirement ages can claim Social Security twice: first as spouses, then using their own work records. A person may choose to sign up for only the spousal benefits at full retirement age and continue accruing delayed retirement credits on his or her own Social Security record. That person can then file for benefits based on his or her own work at a later date and receive a higher monthly benefit, thanks to the delayed retirement credits.

For example, a man planning to retire at age 70 could claim a spouse's benefit based on his wife's earnings at age 66 and then claim again based on his own working record when he exits the work force at age 70. High-income couples with relatively equal earnings gain the most using this strategy, according to calculations by the Center for Retirement Research at Boston College.

4. Include family. Social Security recipients who have children under age 16 or who are disabled can secure additional Social Security payments for the child and a spouse caring for the child, even if the spouse is under age 62. Each child is eligible for up to 50% of the retiree's full benefit. However, payments to family members are capped, typically at 150% to 180% of the retiree's benefit payment. If the total benefits due to the retiree's spouse and children are above this limit, their benefits will be reduced. The retiree's payout is not affected.

5. Take advantage of eligibility for ex-spouses. A former spouse may be eligible for benefits if the marriage lasted at least 10 years. The divorced spouse must be age 62 or older and unmarried. The amount of benefits an ex-spouse claims has no effect on the benefits the worker and his or her current spouse can receive.

6. Boost the survivor's benefit. Widows and widowers are entitled to the higher earner's full retirement benefit. A surviving spouse can begin receiving Social Security benefits at age 60, or at age 50 if he or she is disabled. Benefits are reduced by up to 28.5% if claimed before the recipient's full retirement age. The surviving member of a dual-earner couple also can claim a reduced benefit on one working record and then switch to the other.

For example, a woman could take a reduced widow's benefit at age 60, then, when she reaches full retirement age, claim 100% of the retirement benefits based on her own working record. Most survivor benefits are paid to women because wives are generally younger than their husbands and live longer. A spouse can increase the monthly survivor's benefit by 60% by waiting to sign up for Social Security until age 70.

This article was reported by Emily Brandon for U.S. News & World Report.

DISCLAIMER: No advice, recommendation or solicitation is intended with these posts. Postings here are just topics for discussion. Any investment must be thoroughly researched by you and must be considered in light of your particular circumstances including your current and future obligations, income, stability of income, existing assets, risk tolerance, family situation, age, health, and financial goals. If you need help determining suitability, then please ask

In the first season of "Friends," Rachel Green looks at her first paycheck as a waitress and asks, "Who's this FICA guy, and why is he getting all my money?"

In the first season of "Friends," Rachel Green looks at her first paycheck as a waitress and asks, "Who's this FICA guy, and why is he getting all my money?" There are many ways a married couple can decide to take their Social Security benefits, according to Alicia Munnell, director of the Center for Retirement Research at Boston College. You can't ask Social Security to list them all, so what's the right choice?

There are many ways a married couple can decide to take their Social Security benefits, according to Alicia Munnell, director of the Center for Retirement Research at Boston College. You can't ask Social Security to list them all, so what's the right choice? On the other hand, some people advocate drawing Social Security benefits at the first opportunity.

On the other hand, some people advocate drawing Social Security benefits at the first opportunity. If you're not happy in your marriage after 9 1/2 years, hold off before hiring a divorce attorney.

If you're not happy in your marriage after 9 1/2 years, hold off before hiring a divorce attorney. And we have another dirty little secret for you. If you haven't remarried, chances are your ex-spouse is worth more to you dead than alive -- especially if he or she was a high earner.

And we have another dirty little secret for you. If you haven't remarried, chances are your ex-spouse is worth more to you dead than alive -- especially if he or she was a high earner.  Social Security does a good job of explaining widow and widower benefits, but Dan Keady, director of financial planning for TIAA-CREF Financial Services, says it doesn't clearly spell out a key difference between widow/widower benefits and spousal benefits.

Social Security does a good job of explaining widow and widower benefits, but Dan Keady, director of financial planning for TIAA-CREF Financial Services, says it doesn't clearly spell out a key difference between widow/widower benefits and spousal benefits.

The Social Security website offers an explanation of how your benefits are calculated, but it's a little hard to follow. You can find a simpler explanation at MyRetirementPaycheck.org, a website sponsored by the National Endowment for Financial Education.

The Social Security website offers an explanation of how your benefits are calculated, but it's a little hard to follow. You can find a simpler explanation at MyRetirementPaycheck.org, a website sponsored by the National Endowment for Financial Education.